Definition of Risk: Risk is the possibility of an adverse outcome due to uncertainty. It can be classified into:

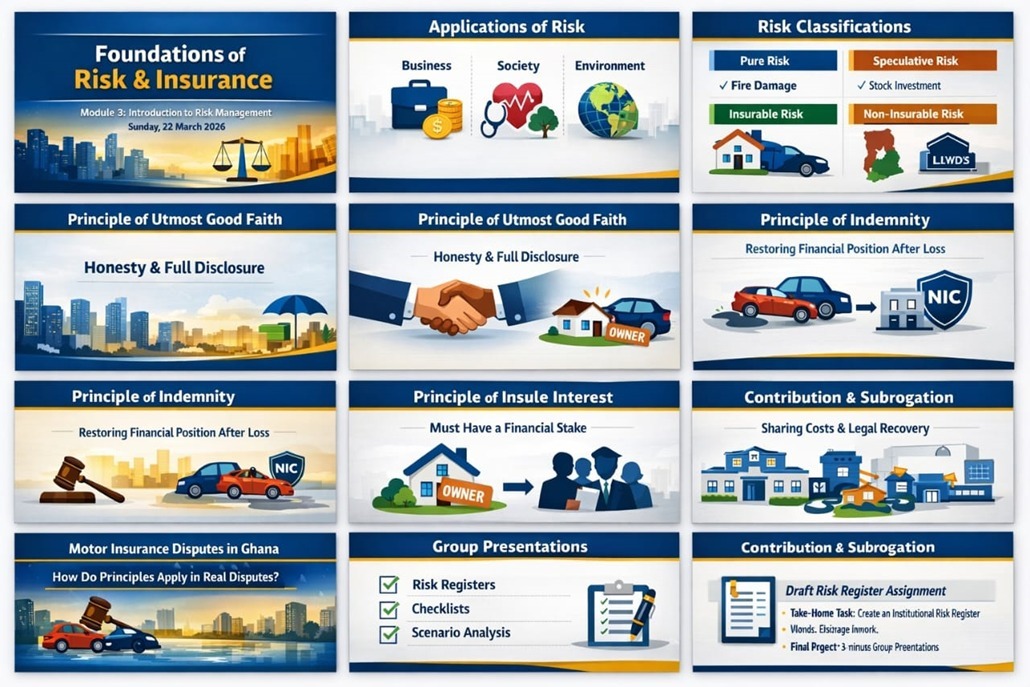

- Pure risk: Only loss or no loss (e.g., fire, theft, illness).

- Speculative risk: Potential for loss or gain (e.g., investments, entrepreneurship).

Types of Risk

- Financial risk: Market volatility, credit defaults.

- Operational risk: Failures in processes, systems, or human error.

- Strategic risk: Poor business decisions or external shocks.

- Compliance/legal risk: Regulatory breaches, lawsuits.

- Environmental/social risk: Natural disasters, reputational damage.

Risk Management Process

- Identification – spotting exposures.

- Assessment – measuring probability and impact.

- Control – prevention and mitigation strategies.

- Financing – transferring risk via insurance or hedging.

- Monitoring – continuous review and adaptation.

Foundations of Insurance

Definition of Insurance

Insurance is a contractual arrangement where risk is transferred from an individual or firm to an insurer in exchange for a premium.

Core Principles

- Pooling of risk: Losses are shared among many policyholders.

- Law of large numbers: Predictability improves with larger insured groups.

- Indemnity: Compensation restores the insured to their pre-loss position.

- Utmost good faith: Both parties must disclose material facts honestly.

- Insurable interest: The insured must stand to suffer a genuine loss.

- Subrogation: Insurer assumes the insured’s legal rights after compensation.

Types of Insurance

- Life insurance: Covers mortality and longevity risks.

- Health insurance: Protects against medical expenses.

- Property insurance: Safeguards physical assets.

- Liability insurance: Covers legal obligations to third parties.

- Reinsurance: Insurers transfer part of their risk to other insurers.

Academic and Professional Relevance

Economic Role: Insurance stabilizes households and firms, enabling sustainable livelihoods despite uncertainty.

Institutional Role: Risk management enhances governance, compliance, and resilience in financial institutions.

Global Context: Postgraduate students must understand how insurance markets interact with international finance, regulation, and development.

Analytical Skills: Quantitative methods (probability, statistics, actuarial science) underpin risk assessment and insurance pricing.

Comparison Table: Risk vs. Insurance Foundations

|

Aspect |

Risk |

Insurance |

|

Nature |

Uncertainty with potential loss

|

Contractual transfer of risk |

|

Classification |

Pure, speculative, financial, etc. |

Life, health, property, liability |

|

Management Approach |

Identify, assess, control, finance |

Pooling, indemnity, subrogation |

|

Key Principle |

Probability & impact analysis |

Utmost good faith, insurable interest |

|

Outcome |

Mitigation or avoidance |

Compensation and stability |

Challenges & Considerations

Moral hazard: Insured parties may act less cautiously.

Adverse selection: High-risk individuals disproportionately seek insurance.

Regulatory compliance: Insurers must meet solvency and reporting standards.

Global risks: Climate change, cyber threats, and pandemics demand innovative insurance solutions.